Outcome-Based Pricing: The End of Shelfware Economics?

Every major software revolution rewrites the rules of value capture. Client-server monetized licenses. SaaS monetized access. AI will monetize outcomes.

Software pricing has always been about value. And every major shift brought it closer to reflecting actual value delivered.

The move from perpetual licenses to subscriptions was real progress. It lowered buyer risk, reduced upfront commitment, and created an entirely new vendor market. Small SaaS companies could acquire customers through self-serve, scale without enterprise sales teams, and grow into major players. The subscription model didn't redistribute the existing market; it disrupted it.

But even usage-based pricing is calculated against planned value, not realized value. You estimate how many seats or API calls you'll need, commit to a contract, and pay whether those resources deliver results or not.

Now AI agents are forcing the next correction: outcome-based pricing, where you pay for results, not resources. And again, the disruption goes well beyond software.

The Physical World Did It First

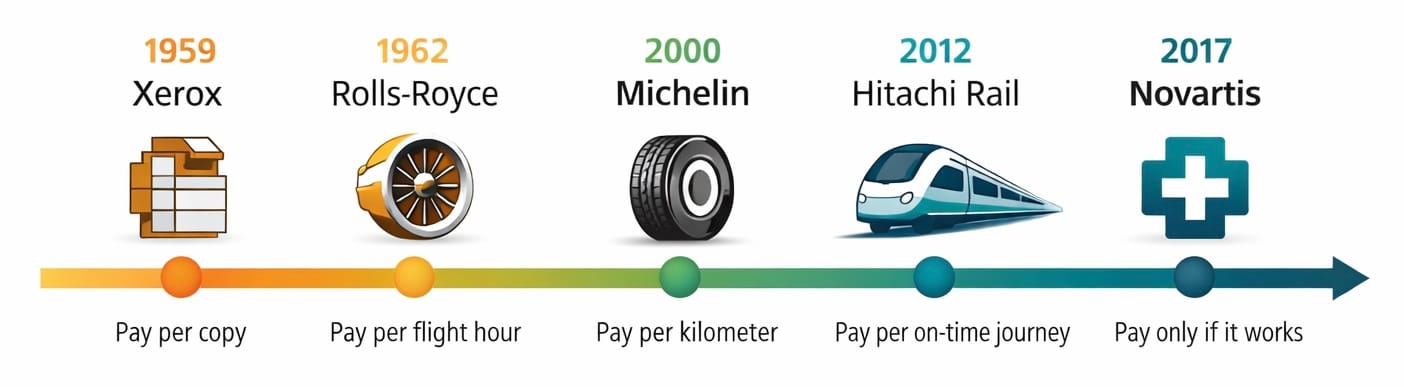

The shift from selling products to selling outcomes started decades ago in the physical world. And the progression tells a story: each model moved one step closer to true pay-for-results.

- 1959. Xerox Model 914: Pay per copy. Rented for $0.10 per copy instead of $27,500 to buy. Unlocked demand nobody predicted: 41% compound annual growth over 12 years, $500 million revenue by 1965.

- 1962. Rolls-Royce "Power by the Hour": Pay per flight hour. Airlines pay for engine uptime, Rolls-Royce retains ownership and bears the maintenance risk. A single Trent engine generates 4x its sale price in service fees over its lifetime. Redefined aerospace economics.

- 2000. Michelin Fleet Solutions: Pay per kilometer. The vendor now profits by making tires last longer, not by selling more of them. Internal conflict nearly killed it; took a separate division with its own IoT platform to resolve. Results: $3 billion+ in annual value created for the trucking industry.

- 2012. Hitachi Rail "Train as a Service": Pay per on-time journey. Hitachi owns and maintains trains in the UK, gets paid only when journeys meet performance KPIs. The pivot point: if the train runs late, Hitachi's revenue takes the hit.

- 2017. Novartis Kymriah: Pay only if it works. The $475,000 CAR-T cancer therapy is charged only when the treatment achieves a clinical response. No response, no charge.

It Ain't About the Price Only, It's About Risk

The common thread isn't pricing alone, it's actually mainly about risk management. At each step, more of it moved from buyer to vendor: maintenance risk (Rolls-Royce), durability risk (Michelin), performance risk (Hitachi), efficacy risk (Novartis). Software has historically lagged here: SLAs guarantee availability, but not outcomes. If the CRM is up 99.9% of the time and nobody closes a deal, that's the customer's problem. AI agents change this equation.

The per-outcome price may look higher than the pay-per-use equivalent since the risk of non-usage and non-performance is factored in. But total spend drops because customers stop paying for capacity they never use.

And successful vendors don't mind managing that risk as part of their product as they move into higher-margin use cases. For example, across all manufacturing, after-sales services represent 25% of revenue but 40-50% of profits (Wharton/Accenture). Outcome-based models shift vendors into the most profitable part of their own value chain.

Software isn't just catching up, it's going further. In the physical world, even the most advanced models struggle with attribution: did the train arrive on time because of Hitachi's maintenance or Network Rail's signaling? In software, AI agents complete discrete, measurable units of work autonomously. The outcome is binary, the attribution is clean, and the vendor either delivered or didn't.

What's Actually Happening in Software

A growing number of software companies are abandoning the usage as their fundamental unit of commerce. Instead, they're charging for what the software actually accomplishes.

Kyle Poyar, a well-known SaaS pricing analyst and author of the Growth Unhinged newsletter, captured the taxonomy well: we're seeing a proliferation of pricing flavors rather than convergence. The progression runs roughly like this:

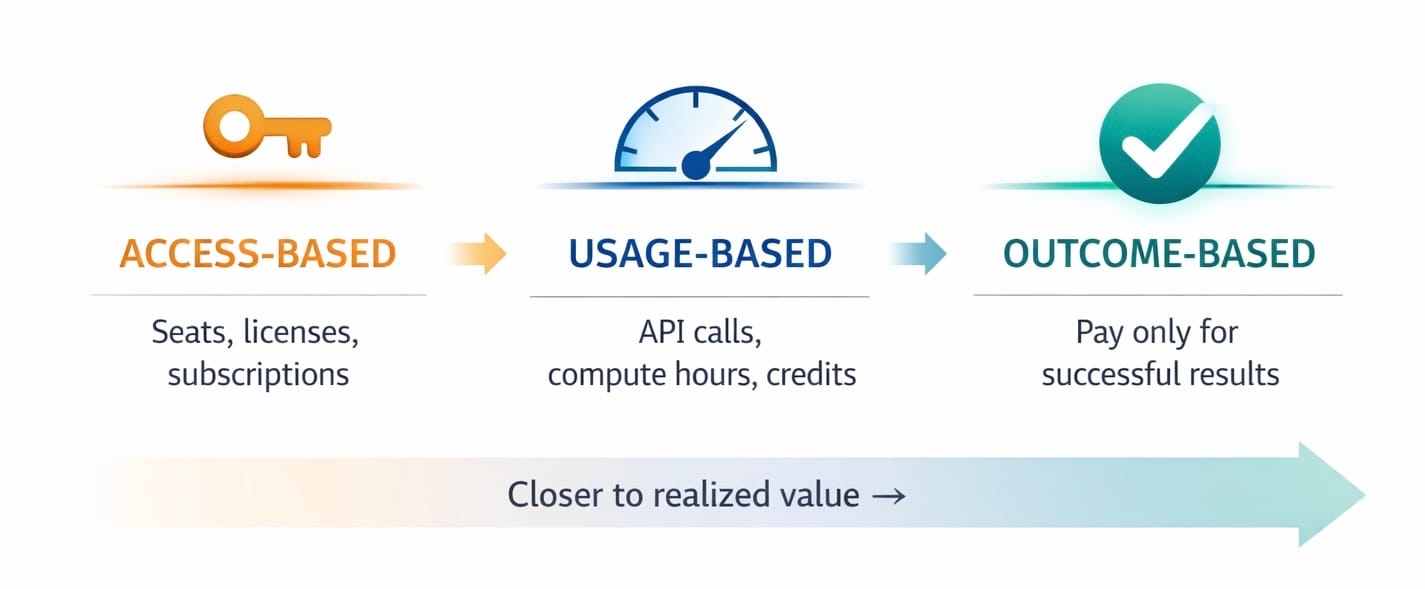

- Access-based: Pay for the right to use (seats, licenses, subscriptions)

- Usage-based: Pay for consumption (API calls, compute hours, credits, actions)

- Outcome-based: Pay only for successful results

Each step moves closer to realized value. And most companies are hedging with hybrids that combine elements from multiple levels. While big vendors like Salesforce struggle to bear the risk and experiment with flavors of usage-based pricing, other software vendors are skipping ahead to outcome-based:

- Zendesk AI: What Zendesk calls resolution-based pricing: pay per resolved support ticket. If the AI can't resolve it, you pay nothing. Adoption is scaling rapidly. The economics are deflationary: as LLM costs drop, Zendesk passes savings through because volume, not price, drives their upside.

- 11x "Alice": AI-powered sales development representative that researches accounts, writes outreach, and books meetings. Priced as a unit of labor against the fully loaded cost of a human SDR. A distinct pattern: AI-as-employee.

- Chargeflow: AI-powered chargeback recovery for e-commerce merchants. Takes a percentage of successfully reversed chargebacks. The vendor only makes money when the customer recovers money. Pure alignment.

- AirHelp: Claims automation platform that handles flight delay and cancellation compensation against airlines on behalf of passengers. Takes a success fee only when the claim is won. No outcome, no fee.

Why Now

LLMs and GenAI agents have come a long way. The speed of innovation is unprecedented. It is still a hard technology to master, but successful companies have achieved it for many use cases.

AI agents can now complete entire units of work autonomously. A customer support interaction. A chargeback dispute. A sales outreach sequence. When the software does the work end-to-end, charging for access to a tool that a human operates makes less sense. You're not selling a tool anymore. You're selling a worker.

But the gap between demo and production is still enormous. Salesforce learned this with Agentforce the hard way: LLMs dropping instructions beyond eight directives, customers discovering that surveys were randomly skipped, and leadership publicly admitting they had "more trust in the LLM a year ago." Salesforce pivoted to "hybrid reasoning," combining LLM flexibility with deterministic rule logic. This is exactly why outcome-based pricing works as a filter. Only vendors whose technology actually delivers reliably can afford to tie revenue to results.

Security is equally unforgiving. In January 2026, researchers disclosed CVE-2025-12420 in ServiceNow's Now Assist platform: a hardcoded credential shared across every customer instance let unauthenticated attackers impersonate any user, including administrators, using only an email address. Once inside, they could weaponize ServiceNow's own AI agents to create backdoor accounts with full privileges. AppOmni called it "the most severe AI-driven vulnerability uncovered to date."

Beyond reliability and security, the economics are shifting too. SaaS companies historically ran at 80-90% gross margins. AI-native products have real variable costs because every inference costs money. Flat subscriptions on top of variable compute don't work, which is why most AI vendors have already moved to usage-based pricing. But buyers are pushing further. They don't want to pay for failed inferences either. They want to pay for results. That's the leap from usage-based to outcome-based.

The physical world shows where this is heading. According to Gartner, outcome-based service contracts in manufacturing jumped from less than 15% of manufacturers in 2018 to over 60% by end of 2022. Software is far behind: McKinsey's 2025 study of 150 global software vendors found that only 2% of incumbents use outcome-based pricing, compared to 10% of AI-native companies. Eighty-six percent of incumbents are still on flat-fee models. The gap between where physical products are and where software is tells you how much runway this trend has.

What Makes Outcome-Based Pricing Work

Not every domain is ready for outcome-based pricing. The models that work well today share a few traits.

- Success is verified by a third party. Vendors can't self-report outcomes. The end customer confirms the support ticket is resolved, the payment processor adjudicates the chargeback, the insurance company validates the billing code. Someone other than the vendor or the buyer decides whether value was delivered.

- The outcome has a known dollar value. A resolved support ticket saves $10-20 in avoided human agent cost. A recovered chargeback has a specific dollar amount. When both sides can do the math, pricing at a fraction of the value created is an easy conversation.

- The billing infrastructure finally exists. You can't invoice for outcomes on Stripe subscriptions. Companies like Metronome and Paid are building the plumbing specifically for outcome-based models. This tooling gap was a real blocker. It's closing.

Where these conditions aren't yet met, hybrid models bridge the gap: a base subscription for platform access, plus a variable component tied to outcomes. Most of the market will live here for a while. The direction matters more than the pace.

The data confirms this is early. Only 17% of enterprise SaaS vendors have implemented true outcome-based pricing (Bain & Company), and only 30% of software firms have published quantifiable ROI from real customer deployments (McKinsey). Meanwhile, AI-enabling a typical customer service stack can mean a 60-80% price increase. Customers are being asked to pay more with less proof. Outcome-based pricing closes that trust gap, but the infrastructure and definitions have to be in place first.

What This Means for the Software Industry

- The shelfware subsidy disappears. In seat-based pricing, unused seats are priced in for everyone. The per-outcome price may look higher, but total spend drops because customers stop paying for capacity they never use.

- Vendor incentives flip. Seat-based vendors optimize for seats sold and churn minimized. Outcome-based vendors optimize for resolution rates and automation quality, because better performance means more revenue.

- A deflationary mechanism kicks in. As foundation models get cheaper, the cost per resolution drops. Outcome-based vendors have a structural incentive to pass savings through because lower prices drive higher volumes.

- Budget flows to proven ROI. When one vendor charges per seat and another charges per result, procurement defends the one tied to outcomes. Outcome-based vendors don't win by selling harder. They win by being the easier line item to justify.

The Broader Pattern

The physical world took 55 years to move from usage-based pricing (Xerox, 1959) to true outcome-based (Hitachi Rail, 2012; Novartis, 2017). Software learned from that playbook and is speed-running the same progression. Salesforce introduced per-user subscriptions in 1999. AWS launched pay-per-hour compute in 2006. By 2024, Zendesk started charging only for successful results. What took the physical world half a century, software compressed into 25 years. And the final leap from usage to outcomes happened in under a decade.

The transition won't be clean. Most of the industry will live in hybrid models for years. Attribution will remain contentious. Revenue recognition will give CFOs headaches. And some domains will remain genuinely hard to price on outcomes because the outcomes are diffuse, delayed, or difficult to measure.

Still: The seat is dead. AI brings the outcome.