The $100 Billion AI Infrastructure Bet That's About to Backfire

While enterprises slash AI budgets and demand real ROI from their pilots, venture capitalists just deployed over $100 billion into AI infrastructure, frontier models, and training capacity. This represents one of the biggest capital allocation mismatches in tech history. VCs are funding the previous generation's playbook—bigger models, more training compute, fancier labs—exactly as enterprises pivot to practical deployment, vendor consolidation, and measurable outcomes.

The disconnect is staggering. Asia Pacific enterprises now demand 2.8x ROI from AI investments while 95% of pilots still fail to reach production. Meanwhile, Anthropic targets a $25 billion round at a $350 billion valuation, xAI closes $20 billion, and infrastructure spending accelerates. These investors are betting on AGI fantasies while real buyers optimize for basic business value.

This collision will define 2026. Either enterprises will suddenly embrace frontier AI capabilities and justify these valuations, or we're witnessing the setup for the largest venture correction since the dot-com crash. The early signals point toward correction, not acceleration.

The Story

The Setup

The AI investment thesis seemed bulletproof: train larger models, build more infrastructure, capture enterprise demand through superior capabilities. VCs poured money into startups promising AGI breakthroughs while enterprises ran pilots to "explore AI transformation." Everyone assumed the gap between cutting-edge research and business deployment would close naturally.

The playbook worked for consumer AI. ChatGPT's viral growth validated the "bigger model, better outcomes" theory. Investors extrapolated this to enterprises, assuming CIOs would pay premium prices for frontier capabilities once they saw the potential.

The Shift

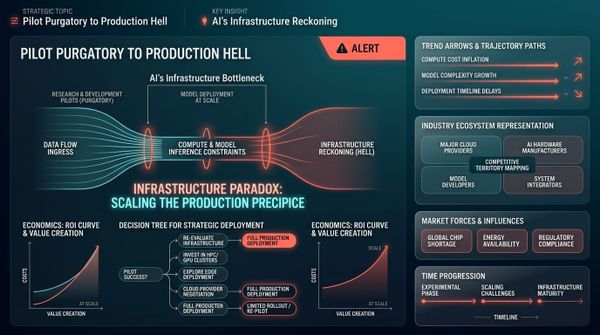

Enterprise reality hit hard in early 2026. Survey data reveals brutal facts: 95% of enterprise AI projects deliver zero measurable ROI, while 40% of agentic AI initiatives face cancellation by end of 2027. Asia Pacific enterprises, despite planning 15% AI budget increases, demand concrete 2.8x returns before deploying capital.

VCs responded by doubling down. Anthropic's $25 billion round, xAI's $20 billion raise, and Skild's $1.4 billion robotics bet represent over $46 billion in fresh capital for experimental AI capabilities. Meanwhile, enterprise buyers consolidate around proven vendors like ServiceNow, Microsoft, and Salesforce for basic productivity gains.

The spending patterns reveal the mismatch: enterprises cut experimental budgets while VCs fund experimental labs.

The Pattern

This mirrors the cleantech crash of 2008-2012, when VCs bet $25 billion on breakthrough energy technologies while utilities demanded incremental improvements. Solar panel efficiency gains and wind turbine optimization delivered real value, but venture-funded fusion and algae biofuels consumed capital without commercial traction.

Today's AI infrastructure investments assume enterprises will eventually pay premium prices for frontier capabilities. But enterprises are moving toward vendor consolidation, not capability expansion. ServiceNow's OpenAI partnership signals the winning strategy: embed proven AI into existing workflows rather than replace them with experimental agents.

The capital flowing into training infrastructure and model development addresses yesterday's bottlenecks. Enterprises now face deployment challenges: data quality, integration complexity, change management, and ROI measurement. These problems require software engineering discipline, not research breakthroughs.

The Stakes

If enterprises don't accelerate AI adoption by Q3 2026, these valuations become unsustainable. Anthropic at $350 billion needs to capture significant enterprise market share from Microsoft and Google. That requires not just better models, but better enterprise sales, support, integration, and deployment capabilities—areas where incumbents dominate.

The alternative scenario—rapid enterprise acceleration—requires solving practical problems VCs aren't funding. Data engineering automation (Microsoft's Osmos acquisition), inference optimization (NVIDIA's Baseten investment), and workflow integration (ServiceNow partnerships) matter more than training larger models.

Energy constraints compound the problem. OpenAI's renewable energy deals and hyperscale data center investments lock capital into fixed infrastructure before demand materializes. If enterprises consolidate around fewer vendors, this infrastructure becomes stranded assets.

What This Means For You

For CTOs

Stop evaluating frontier AI capabilities and focus on integration infrastructure. By Q2, audit your current AI pilot ROI and consolidate around vendors that integrate with existing systems. Microsoft's Fabric ecosystem and ServiceNow's platform approach will capture more enterprise value than standalone AI tools.

Negotiate renewable energy partnerships now if you're planning significant AI infrastructure. Energy procurement has become a competitive moat as hyperscalers lock up capacity. Consider hybrid architectures that balance cloud AI services with on-premises inference to control costs and latency.

Prepare for vendor consolidation acceleration. The experimental phase ends this year—choose AI vendors that can survive enterprise procurement cycles and deliver measurable business outcomes, not impressive demos.

For AI Product Leaders

Abandon the "better model" product strategy immediately. Enterprise buyers want integration depth, not capability breadth. Focus product development on seamless workflow embedding rather than standalone AI experiences.

Partner with established enterprise software vendors rather than competing directly. The ServiceNow-OpenAI model will proliferate as platform companies acquire AI capabilities to strengthen customer retention rather than expand TAM.

Price for deployment economics, not training costs. Inference optimization and real-time decision-making will differentiate products more than model sophistication as enterprises scale beyond pilots.

For Engineering Leaders

Shift infrastructure investment from training capacity to inference optimization. Real-time AI deployment, not model development, determines production success. Invest in data engineering automation and integration platforms that accelerate time-to-value.

Build for hybrid architectures that combine cloud AI services with edge inference. Energy costs and latency requirements will force distributed deployment models as enterprises scale AI beyond experimental use cases.

Hire for enterprise integration skills over AI research capabilities. The bottleneck has moved from model development to production deployment, requiring different engineering expertise.

What We're Watching

Anthropic's enterprise traction by Q2 2026: If the company can't demonstrate significant Fortune 500 wins beyond pilot programs, the $350 billion valuation becomes indefensible.

Energy infrastructure utilization rates: OpenAI and competitors are making massive power commitments. If enterprise demand doesn't materialize, these become stranded costs that crater unit economics.

Microsoft's AI infrastructure consolidation: The company's Osmos acquisition signals a shift toward practical deployment tools. Watch for additional acquisitions that prioritize integration over innovation.

Enterprise AI vendor rationalization: VCs predict enterprises will consolidate around fewer vendors by mid-2026. The speed and severity of this consolidation will determine which startups survive.

Q2 enterprise AI budget reallocations: If the trend toward consolidation accelerates, experimental AI budgets will shift to proven platforms, starving late-stage startups of customer acquisition opportunities.

The Bottom Line

The great venture-enterprise disconnect of 2026 resolves one way: either enterprises rapidly adopt frontier AI capabilities to justify current valuations, or the largest AI funding correction in history begins by summer. Early indicators favor correction over acceleration. The 95% pilot failure rate, enterprise consolidation trends, and focus on practical deployment over capability expansion suggest VCs are funding the wrong layer of the stack. Mark your calendars for June 2026—that's when unsustainable burn rates meet enterprise budget reallocations. The survivors won't be the companies with the biggest models or most funding. They'll be the ones solving deployment problems enterprises actually face.